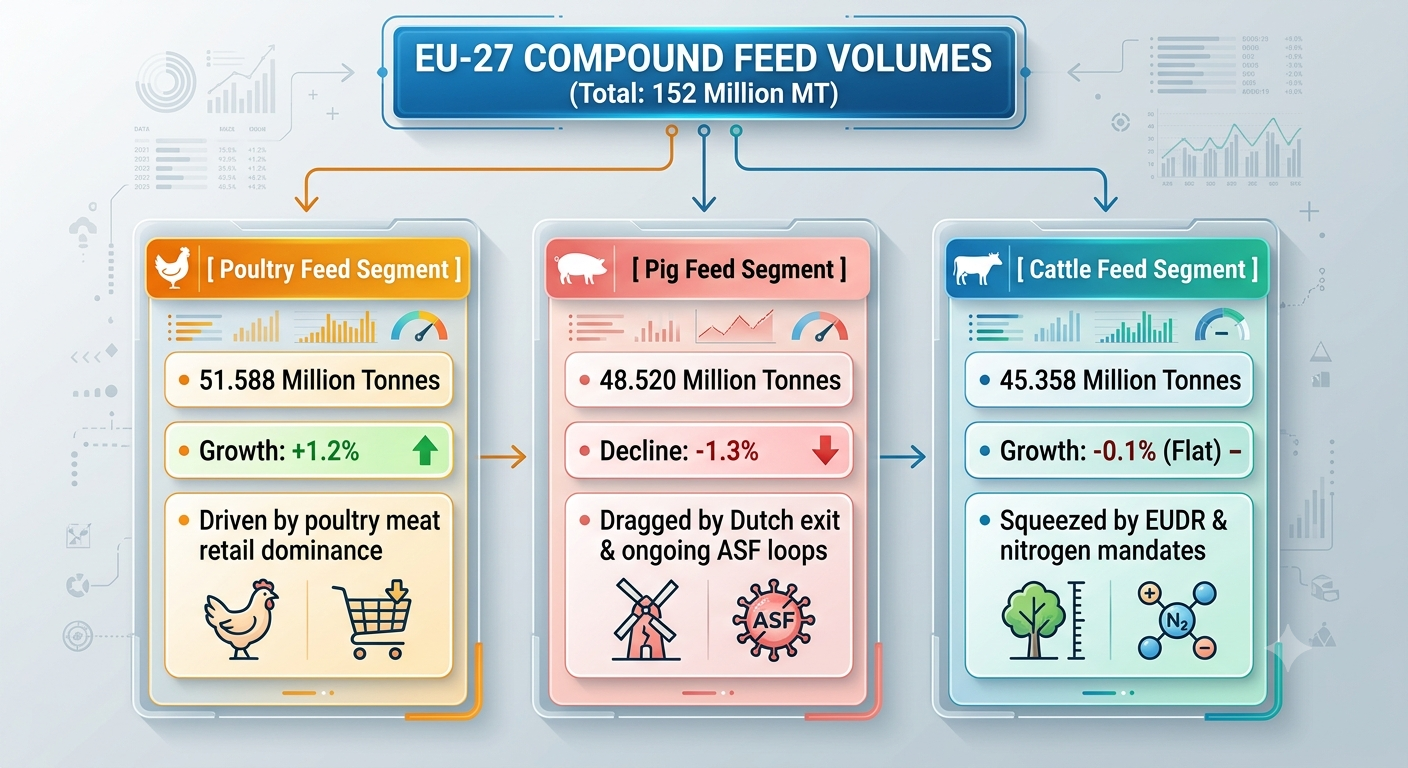

According to official data and market forecasts compiled by the European Compound Feed Manufacturers’ Federation (FEFAC), total industrial compound feed production across the EU-27 is projected to hit 152 million tonnes, representing a nominal year-on-year contraction of just 0.06% compared to last year.

While this macro-level metric suggests structural stability across Europe’s agrifood supply lines, an open analysis of the data reveals a sharply polarized marketplace. A booming poultry meat sector is serving as the primary commercial engine keeping mill volumes afloat, directly counterbalancing a structural contraction in the swine corridor and defensive consolidation in the dairy and beef segments.

The total EU footprint of 152 million tonnes is divided into three core livestock processing streams, driven by diverging consumer behavior, pathogen pressures, and state-level green initiatives.

Livestock Segment

|

Projected Production (Metric Tonnes)

|

Year-on-Year Growth Rate (%)

|

Primary Macro Drivers

|

Poultry Feed

|

51.588 Million

|

+1.2%

|

Robust domestic retail demand; superior Feed Conversion Ratios (FCR).

|

Pig Feed

|

48.520 Million

|

-1.3%

|

Structural herd reductions; African Swine Fever (ASF) culling; nitrogen rules.

|

Cattle Feed

|

45.358 Million

|

-0.1%

|

Environmental regulatory enforcement (EUDR); volatile farmgate milk prices.

|

Total EU-27 Market

|

152.000 Million

|

-0.06%

|

Diverging country-level policy performance.

|

Poultry Feed: Remains Growth Engine

Poultry feed is the only major species sector registering positive expansion, climbing 1.2% to secure its spot as Europe’s highest-volume feed category. This growth reflects a long-term consumer shift toward poultry as an affordable, lean protein source amidst Eurozone inflationary pressures. Top Performing National Corridors

-

Germany (+3.8%): Leading industrial integration setups have heavily expanded broiler grids to substitute volatile pork volumes.

-

Poland (+3.0% to 7.46M tonnes): Solidifying its status as Europe’s low-cost poultry exporter hub.

-

Spain (+2.0%): Strong domestic retail performance and highly optimized mill integration lines.

-

France (+1.5% to 8.250M tonnes): Rebuilding capacity after previous migratory bird waves.

Epidemiological Headwinds: While expansion is strong, the poultry grid faces constant biological stress from Highly Pathogenic Avian Influenza (HPAI). Recurrent outbreaks along wild migratory bird flyways require strict localized quarantine loops, limiting the sector’s total volume potential.

Pig Feed: Structural Decline and Pathogen Drag

The pig feed segment continues to show the most vulnerability, dropping 1.3% to 48.520 million tonnes. This contraction stems from an ongoing structural resizing of Northwest Europe’s porcine herd, driven by a combination of strict state environmental buy-out programs and active pathogen zones. Pronounced Regional Contractions

-

The Netherlands (-10.0%): The steepest drop in the EU, triggered directly by state-funded farm closures aimed at curbing localized nitrogen and ammonia emissions.

-

Spain (-1.5% to 13.1M tonnes): Though it remains Europe’s largest single pig feed producer, high raw material input costs have forced a marginal correction in herd numbers.

-

Germany & France (-1.0%): Declining consumer demand for pork and rising operational compliance costs continue to shrink internal breeding bases.

Eastern Pockets of Resilience

In contrast to the western contraction, Poland (+3.0%) and Bulgaria (+5.8%) are registering solid gains. These nations are aggressively modernizing legacy facilities into automated, highly biosecure commercial units capable of managing the constant pressure of African Swine Fever (ASF).

Cattle Feed: Defensive Alignment and Regulatory Friction

At 45.358 million tonnes, EU cattle feed production remains functionally flat (-0.1%), masking significant policy-driven friction at the national level.

Western Environmental Attrition

The Benelux region is bearing the brunt of Europe’s new green agricultural paradigm. The Netherlands (-5.0%) and Belgium (-2.0%) are seeing sharp mill volume drops. This is a direct consequence of strict national environmental regulations targeting manure output, paired with depressed dairy farmgate milk prices that discourage intensive supplementary feeding.

Southern and Eastern Equilibrium

Conversely, Spain (+2.0%) expects growth thanks to expanded beef export channels, while France and Poland are holding stable. This geographic shift is altering the demand for raw ingredients across European feed mills

Macro Uncertainties: What is Driving Volatility?

FEFAC’s market tracking highlights three systemic friction points that feed mill operators must navigate through the remainder of the year:

1. The EU Deforestation Regulation (EUDR) Implementation

The impending enforcement of strict traceability guidelines for imported soy has introduced significant administrative and compliance burdens. Feed formulators are scrambling to secure certified, geo-mapped soybean meal streams, driving up the baseline cost of high-protein formulations.

2. High Upstream Operational Costs

While crop prices have backed off from their historical peaks, feed millers remain highly vulnerable to volatile energy and fertilizer markets. These inputs directly impact the overhead costs of grain drying, pelleting, and logistics.

3. Precision Feed Formulation Shifts

Faced with shrinking margins in the pig and cattle lines, the European market is pivoting heavily toward precision animal nutrition. Advanced software integration is allowing feed mills to rely on low-carbon alternative raw materials—including local co-products like brewers’ grains, sugar beet pulp, and specialty synthetic amino acids—to maintain strict performance targets while lowering reliance on volatile international grain imports.

MARKET FORECASTS & PROJECTIONS – 2026-2027 Outlook

| Sector |

5-Year Trend |

Primary Driver |

| Poultry |

Upward growth |

Protein demand |

| Pig |

Downward pressure |

ASF + regulation |

| Cattle |

Stable/declining |

Environmental policy |

| Overall |

Slight decline |

Mixed sector performance |

KEY TAKEAWAYS – For Industry Stakeholders

-

Overall Stability: EU27 total feed production remains largely stable at 152 million tonnes (-0.06%)

-

Poultry Growth: Poultry feed is the primary growth driver with +1.2% growth forecast

-

Pig Decline: Pig feed faces significant challenges with -1.3% decline due to ASF

-

Cattle Stability: Cattle feed remains largely stable with slight reductions from environmental policies

-

Disease Pressure: African Swine Fever continues to have detrimental effect on pig sector

-

Regulatory Impact: Environmental policies shaping cattle feed production levels

-

Market Forecast: Marginal overall decrease masks significant sector divergence

{kind=link}