{kind=link}

Most comprehensive report on Global Methane Gas Inhibitors being developed / commercialised in Cattle – Dairy and Beef segment.

One of the newest innovations to be launched in world’s cattle markets, Methane inhibitors have emerged as the fastest-growing segments within animal nutrition, climate technology and livestock sustainability purely on account of varied benefits to multiple stakeholders.

Enteric methane generated by cattle contribute significantly to agricultural greenhouse gas emissions globally and roughly 5–6% of total anthropogenic greenhouse gas emissions, making methane reduction as one of the highest-priority perceived climate interventions in livestock production.

The sector has moved rapidly from academic research into commercial deployment over last more than 2 years, driven by:

-

Net-zero commitments from dairy and beef companies

-

Carbon reduction regulations

-

ESG-linked financing

-

Carbon credit programs

-

Corporate sustainability targets

Industry analysts estimate the global methane mitigation market for ruminants could exceed US$3–5 billion annually by 2035, with feed additives leading the way ahead.

Global Cattle Population

Region |

Cattle Population (Million Head) |

|---|---|

India |

~307 |

Brazil |

~238 |

China |

~102 |

United States |

~87 |

EU-27 |

~74 |

Argentina |

~54 |

Australia |

~29 |

Rest of World |

~760 |

Global Total |

~1.65 billion |

Source: FAO, USDA, national livestock databases.

Enteric Methane Emissions -Average methane production:

Animal Type |

Methane Emissions |

|---|---|

Dairy Cow |

100–140 kg CH₄/year |

Beef Cattle Feedlot |

50–80 kg CH₄/year |

Grazing Beef Cow |

70–120 kg CH₄/year |

Methane possesses approximately 28–34 times the warming potential of carbon dioxide over a 100-year timeframe, hence so much interest in methane gas inhibitors.

Global Methane Inhibitor Market

Year |

Estimated Market Value |

|---|---|

2024 |

US$290 million |

2025 |

US$370 million |

2026 |

US$470 million |

2030 |

US$1.4 billion |

2035 |

US$3–5 billion |

Estimated CAGR: 25–35%

Leading Commercial Methane Inhibitor Products

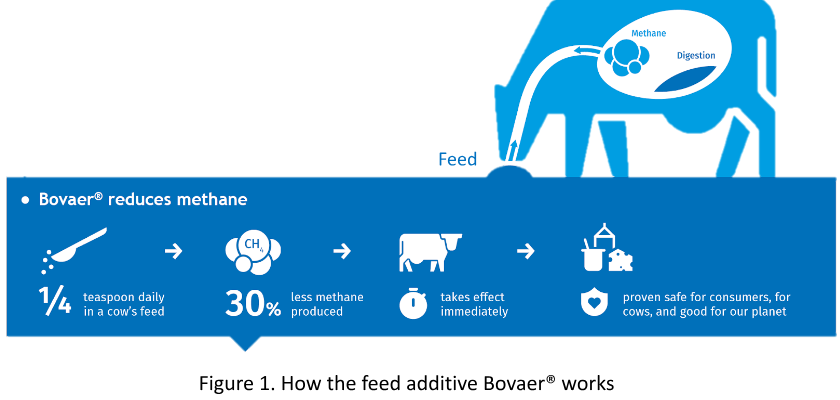

1. Bovaer (DSM-Firmenich)

Active Ingredient – 3-Nitrooxypropanol (3-NOP)

Innovator: DSM-Firmenich

Marketer: Elanco Animal Health

Mechanism – Blocks methyl-coenzyme M reductase, the final enzyme responsible for methane production inside the rumen.

Efficacy

Trial Type |

Reduction |

|---|---|

Dairy Cattle |

20–45% |

Feedlot Beef |

30–45% |

Intensive Systems |

Up to 50% |

Commercial Status – Approved in:

-

European Union

-

United Kingdom

-

Australia

-

Brazil

-

Chile

-

Canada

-

Several Latin American markets

Regulatory submissions continue globally.

Global Revenues of Bovaer

DSM has not separately disclosed Bovaer revenue, but industry estimates suggest:

Metric |

Estimate |

|---|---|

2025 Revenue |

US$40–60 million |

2030 Revenue Potential |

US$500 million+ |

2. Rumin8

Country – Australia

Rumin8 Technology – Synthetic production of bioactive compounds inspired by seaweed-derived methane inhibitors.

Key Advantages:

-

Scalable fermentation

-

Lower cost than harvesting seaweed

-

Easier integration into feed systems

Major Investors

-

Breakthrough Energy Ventures

-

Australian venture funds

-

Strategic livestock investors

Recent Data – 2026 Brazil feedlot study:

Parameter |

Result |

|---|---|

Methane Reduction |

50.4% |

Feed Efficiency Improvement |

5% |

The study was conducted with Minerva Foods and the University of São Paulo.

3. FutureFeed

Country – Australia

FutureFeed Core Technology – Asparagopsis seaweed.

Methane Reduction

Trial |

Reduction |

|---|---|

Dairy |

60–80% |

Feedlot |

70–90% |

Highest efficacy demonstrated among commercially available products.

Challenge – Scaling seaweed cultivation

Current bottlenecks:

-

Biomass production

-

Harvest logistics

-

Cost per animal

4. Mootral

Country – Switzerland

Mootral Technology – Natural garlic extracts + citrus compounds.

Methane Reduction – 15–30%

Target market:

-

Organic dairy

-

Natural beef production

-

Premium sustainability programs

5. Agolin

Country – Switzerland

Agolin Technology – Essential oil blend.

Reported Reduction – 5–20%

Strong adoption in:

-

Dairy systems

-

Carbon programs

-

Sustainability certification schemes

Competitive Landscape

Company |

Technology |

Reduction |

|---|---|---|

DSM-Firmenich |

3-NOP |

20–50% |

FutureFeed |

Asparagopsis |

60–90% |

Rumin8 |

Synthetic bioactive |

30–60% |

Mootral |

Garlic-citrus |

15–30% |

Agolin |

Essential oils |

5–20% |

Symbrosia |

Seaweed |

50–80% |

CH4 Global |

Seaweed |

60–90% |

Market Segmentation

Segment |

Share |

|---|---|

Dairy Cattle |

62% |

Beef Feedlot |

24% |

Grazing Beef |

11% |

Sheep & Goats |

3% |

Dairy remains the largest commercial opportunity due to controlled feeding systems.

Geographic Opportunity

Largest Future Markets

Country |

Opportunity |

|---|---|

EU |

Regulatory-driven |

New Zealand |

Methane mandates |

Australia |

Export sustainability |

United States |

Corporate ESG |

Brazil |

Beef exports |

Canada |

Dairy sustainability |

Economics at Farm Level

Typical Bovaer economics:

Metric |

Value |

|---|---|

Cost per Cow/Day |

US$0.05–0.12 |

Annual Cost/Cow |

US$18–45 |

Carbon Reduction |

1–1.5 tonnes CO₂e/year |

Potential carbon credit value:

US$20–80 per cow annually depending on market.

Carbon Credit Opportunity – Major buyers include:

-

Dairy processors

-

Retailers

-

Food companies

-

Sustainability funds

M&A and Investment Activity

Major investors entering the sector include:

-

Breakthrough Energy Ventures

-

Temasek

-

Lowercarbon Capital

-

Tyson Ventures

-

Cargill

-

JBS

Total disclosed venture and strategic investment in methane-reduction technologies has exceeded US$500 million over the past five years.

Key Risks

-

Regulatory – Approval pathways remain complex in several markets.

-

Cost – Large-scale adoption depends on maintaining favorable economics.

-

Grazing Systems – Most technologies work best in feedlots and dairy farms. Pasture-based cattle remain difficult to address.

-

Supply Chain – Seaweed-based solutions face production constraints.

Outlook to 2035

Methane inhibitors are expected to become a standard component of intensive dairy and beef production in many developed markets. Industry forecasts suggest:

Metric |

2035 Projection |

|---|---|

Treated Cattle |

250–400 million head |

Market Value |

US$3–5 billion |

CO₂e Reduction |

500+ million tonnes annually |

Leading Segment |

Dairy cattle |